Why Cost Per Wallet Matters More Than Ever in 2026?

Crypto didn’t run out of users in 2025. It ran out of excuses. With VC funding down 98% from its 2021 peak as noted by @WClementeIII, crypto growth is forced into a revenue-first reality. In that environment, Cost Per Wallet (CPW) isn’t a growth metric. It’s a filter for whether a business survives in crypto.

CPW is the cost of getting a verified crypto user on your website: someone who already has a crypto wallet installed, not just a click, a session, or generic traffic, which based on prior research shows 7x higher chances of conversions in crypto. CPW doesn’t replace revenue or LTV, but it surfaces acquisition friction earlier than almost any downstream metric. When CPW breaks, unit economics usually follows. For more context read the article here.

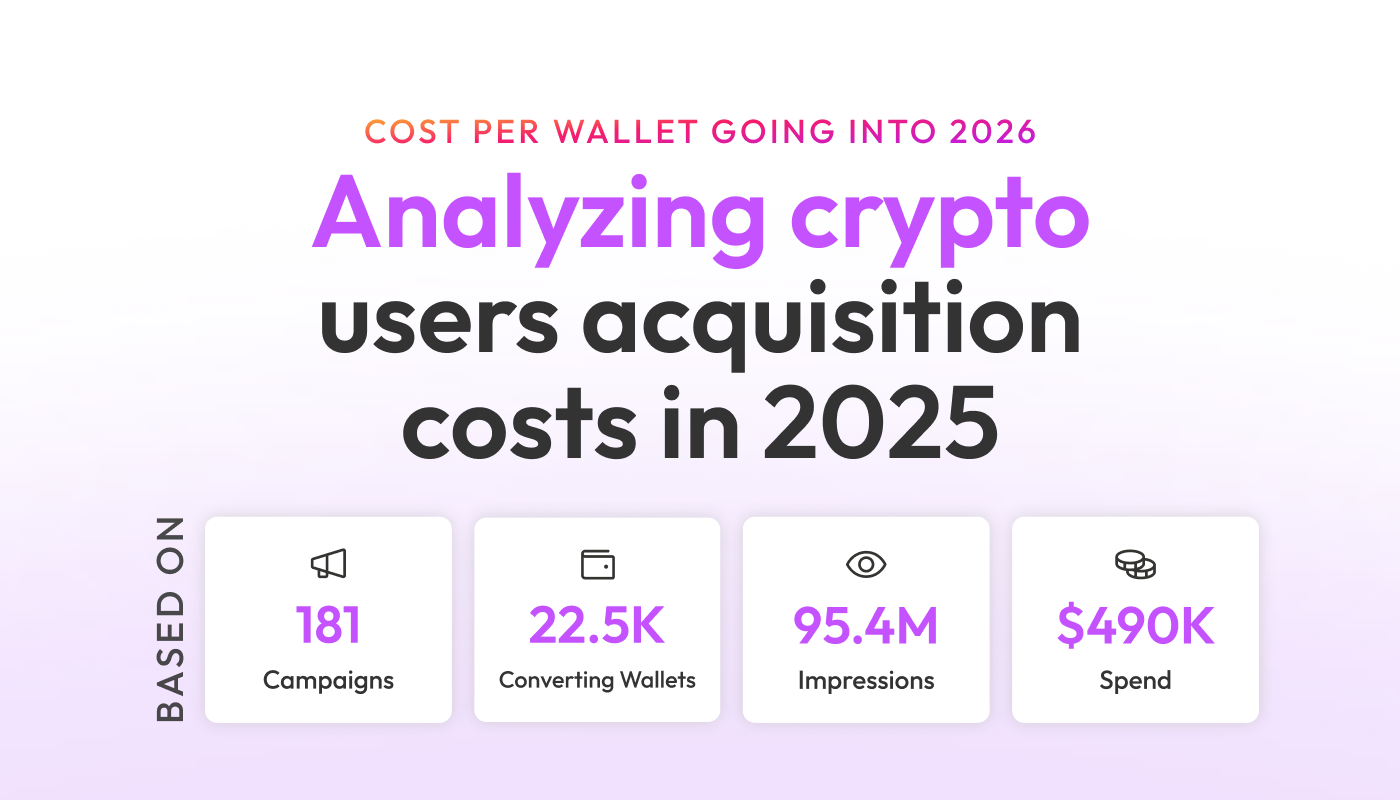

This article examines what CPW revealed in 2025 and why it may be the clearest signal for how crypto growth will be won or lost going into 2026. The analysis is based on a subsample of Addressable data covering 45 advertisers, 181 web banner campaigns, $490k in spend, 95.4M impressions, and 22.4k unique wallet-bearing users acquired.

CPW mattered more in 2025 for three reasons:

1. Crypto shifts to revenue-first reality: As VC attention snapped toward AI, new crypto startup formation and VC funding slowed, pushing crypto businesses into a revenue-first reality almost overnight. Growth teams stopped optimizing for attention and started being judged on unit economics. CPW went from interesting to existential.

2. Crypto users have decoupled from the crypto industry itself.

While new crypto companies and VC funding slowed, users did not. Monthly active onchain users reached an all-time high of ~70M, as highlighted by @a16zcrypto.

Heading into 2026, this increasingly affluent base controls over $1.7T in assets, a figure inferred from @coindesk data showing ~71.8% of Bitcoin held by retail investors. And that scale matters beyond crypto-native companies as TradFi, iGaming, and luxury brands can now (finally) activate crypto users directly, with players like @stripe and @paypal enabling crypto-to-fiat payments, and banks like @jpmorgan, @goldmannsachs, and @hsbc making crypto balances usable in real-world commerce.

3. CPW reporting became materially more accurate: In 2024, CPW was reported at the session level: a website visit that included a wallet was counted, even if the same user returned multiple times. In 2025, @addressable improved its identity resolution and user fingerprinting, allowing us to recognize returning users and avoid overcounting. This didn’t change CPW as a metric, but it significantly improved advertisers’ ability to understand what CPW actually represents: the cost of acquiring a unique user with a wallet.

Also, as Addressable scaled its managed spend in 2025 more than 4x, the dataset behind this report expanded, enabling broader regional coverage and more reliable CPW benchmarks.

Ultimately, the goal is clarity: What did crypto acquisition actually look like in 2025 compared to 2024? And did crypto retail disappear, or did it simply outgrow the crypto industry itself?

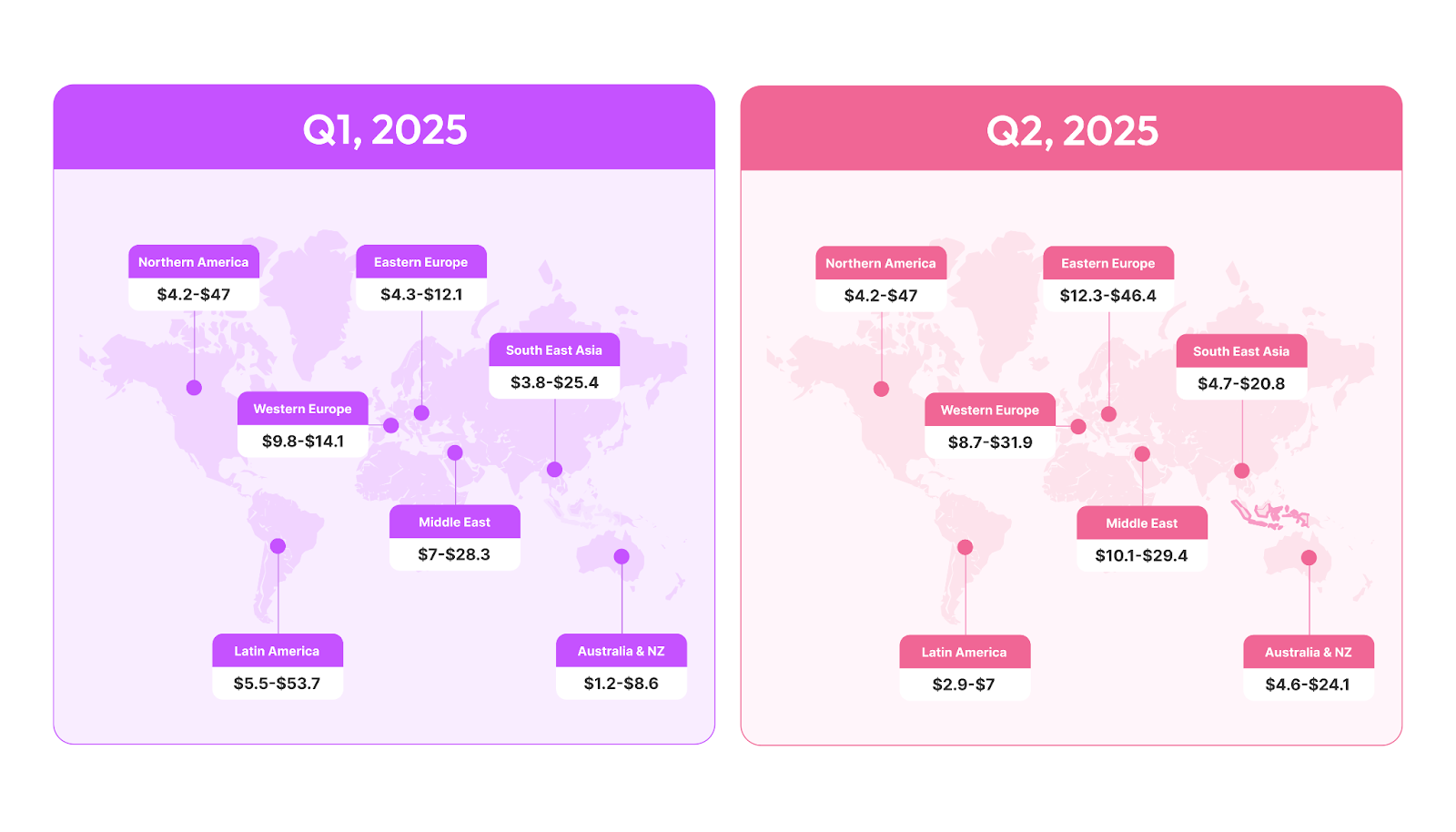

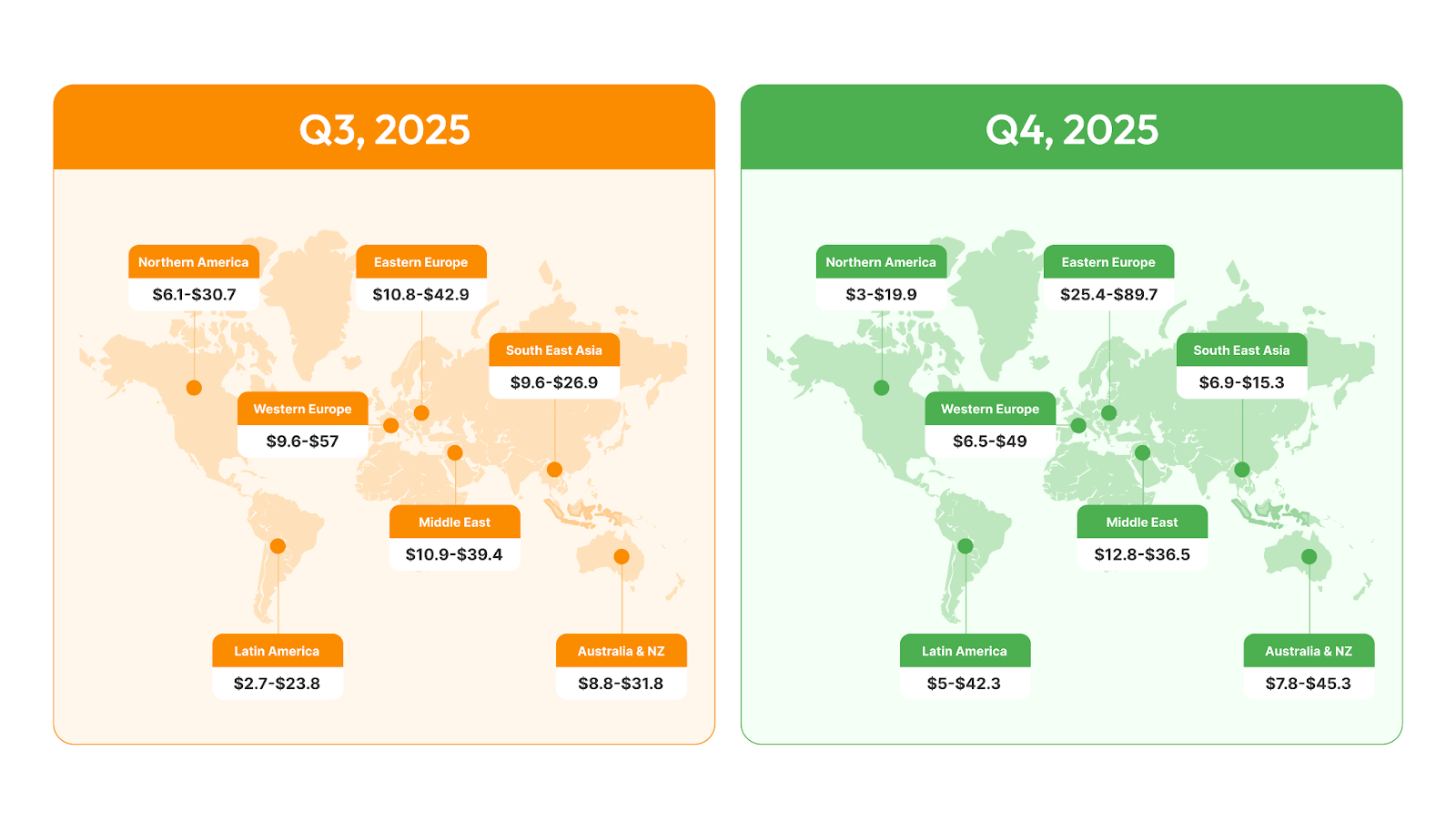

CPW by Geography in 2025: Premium Got Predictable, Emerging Got Rational

In 2025, retail crypto slowed and organic user inflow thinned, while competition intensified as startups were pushed into a revenue-first reality. Advertisers stopped experimenting and started optimizing under real economic pressure. At Addressable, we witnessed media budgets scaling 4x YoY, expanding regional coverage and producing far cleaner signals. The result is straightforward economics: more budget competing for roughly the same pool of crypto users, and higher CPW.

You see this most clearly in premium regions. Western Europe and North America became meaningfully more expensive, often 2-3x higher than reported results in 2024, but the more important change was stability. CPW moved into higher, tighter bands with far fewer quarter-to-quarter swings. Costs went up, but volatility collapsed. That combination signals maturity. Premium crypto users stopped behaving like speculative bursts and started behaving like a durable, repeatable audience.

Emerging regions tell the other half of the story. As revenue-focused advertisers concentrated on premium markets chasing monetization, competitive pressure eased elsewhere. South-East Asia and LATAM didn’t collapse. They reset. CPW ranges narrowed and shifted downward through 2025 as speculative, short-term budgets exited. What remained was more sustainable pricing driven by advertisers who actually intend to stay. For teams looking to validate PMF or build early traction, these regions quietly became more attractive again.

So what is going into 2026?

- Geography is no longer just a scaling decision. It’s a unit-economics lever. Premium regions increasingly function as revenue engines, where higher CPW can make sense once monetization is proven. Emerging regions offer a more efficient path to learning, iteration, and initial user acquisition.

- At the same time, targeting quality now plays a decisive role. As crypto users mature and competition intensifies, the difference between broad, undifferentiated buying and precise user-level targeting can easily translate into 3-10x differences in CPW, often determining whether a market is genuinely expensive or simply expensive by execution.

These aren’t rigid rules. But they define the trade-offs growth teams will increasingly be forced to navigate as crypto acquisition becomes less speculative and far more economics-driven heading into 2026.

Figure 1: The interquartile range (P25–P75) for each region and quarter, capturing where most campaigns are actually priced while filtering out extreme outliers.

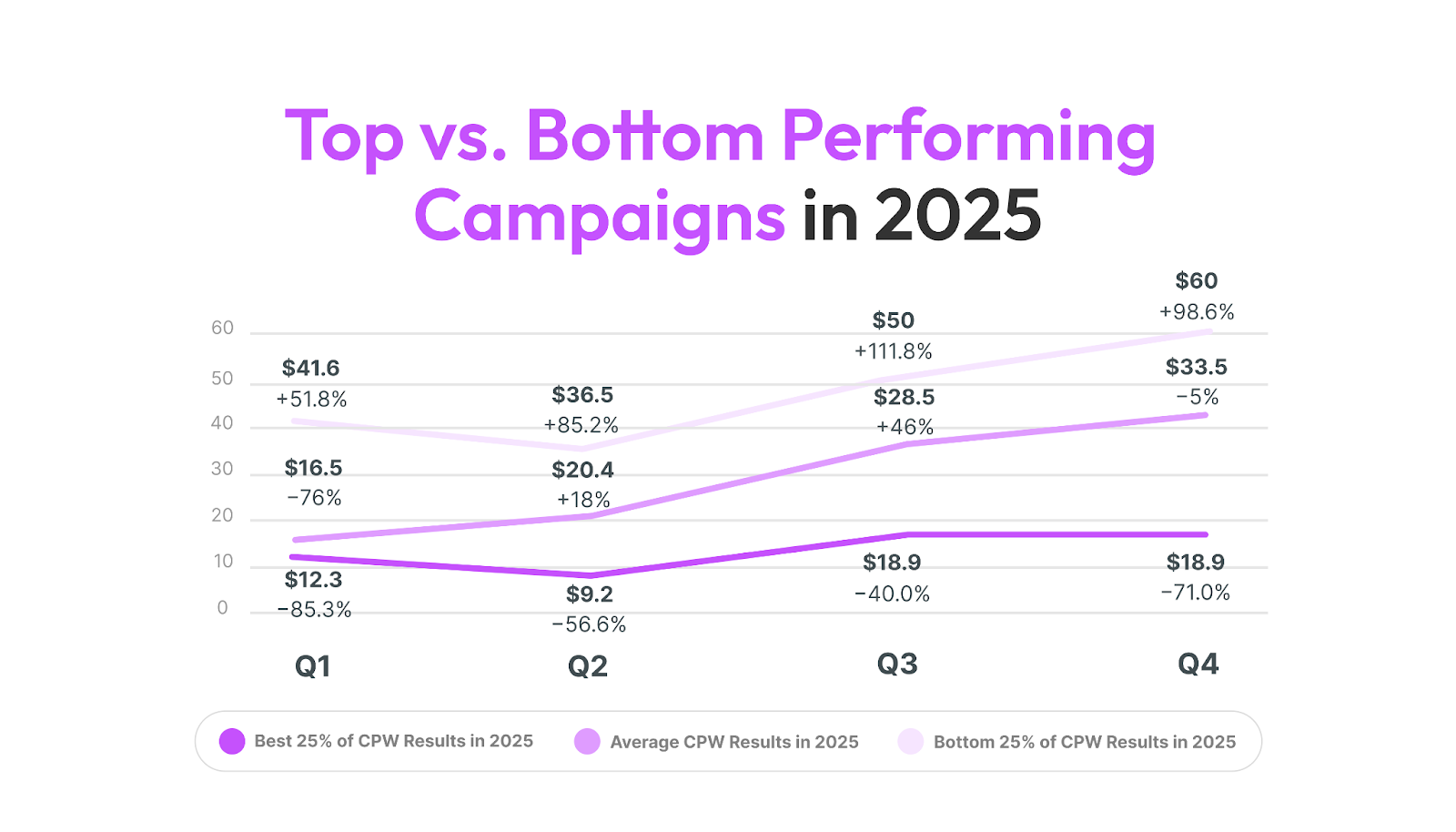

Strong Brands Pay Less. Everyone Else Pays x2–3 More

Before getting into the results, a quick note on how this was done. Instead of ranking individual campaigns, we grouped performance at the advertiser level. Advertisers were ranked by CPW, and we focused on the top 25% and bottom 25% to reduce noise. All campaigns from each advertiser inherited that rank. This way, the comparison reflects brand strength, not one-off campaign tactics.

Once you look at the data through that lens, the pattern is hard to miss. Strong brands acquired users for less. In many cases, the top advertisers, large centralized exchanges, leading iGaming and trading platforms, paid less in 2025 than they did in 2024, despite a tougher market. Meanwhile, unknown or early-stage crypto startups routinely paid x2 more to acquire the same type of user.

This exposes a common misconception. Many crypto startups try to cut corners by skipping brands and going straight to CPA / FTD campaigns. In practice, that makes acquisition more expensive. When users don’t recognize or trust you, performance marketing has to do everything: introduce the brand, build credibility, explain risk, and convince them to act. That extra friction shows up immediately as higher CPW.

In 2024, hype helped mask this gap. In 2025, it didn’t.

CPW makes the tradeoff explicit: brand isn’t a “nice-to-have.” It’s a cost advantage.

Figure 2: Quarterly CPW in 2025 for the top 25%, average, and bottom 25% of advertisers.

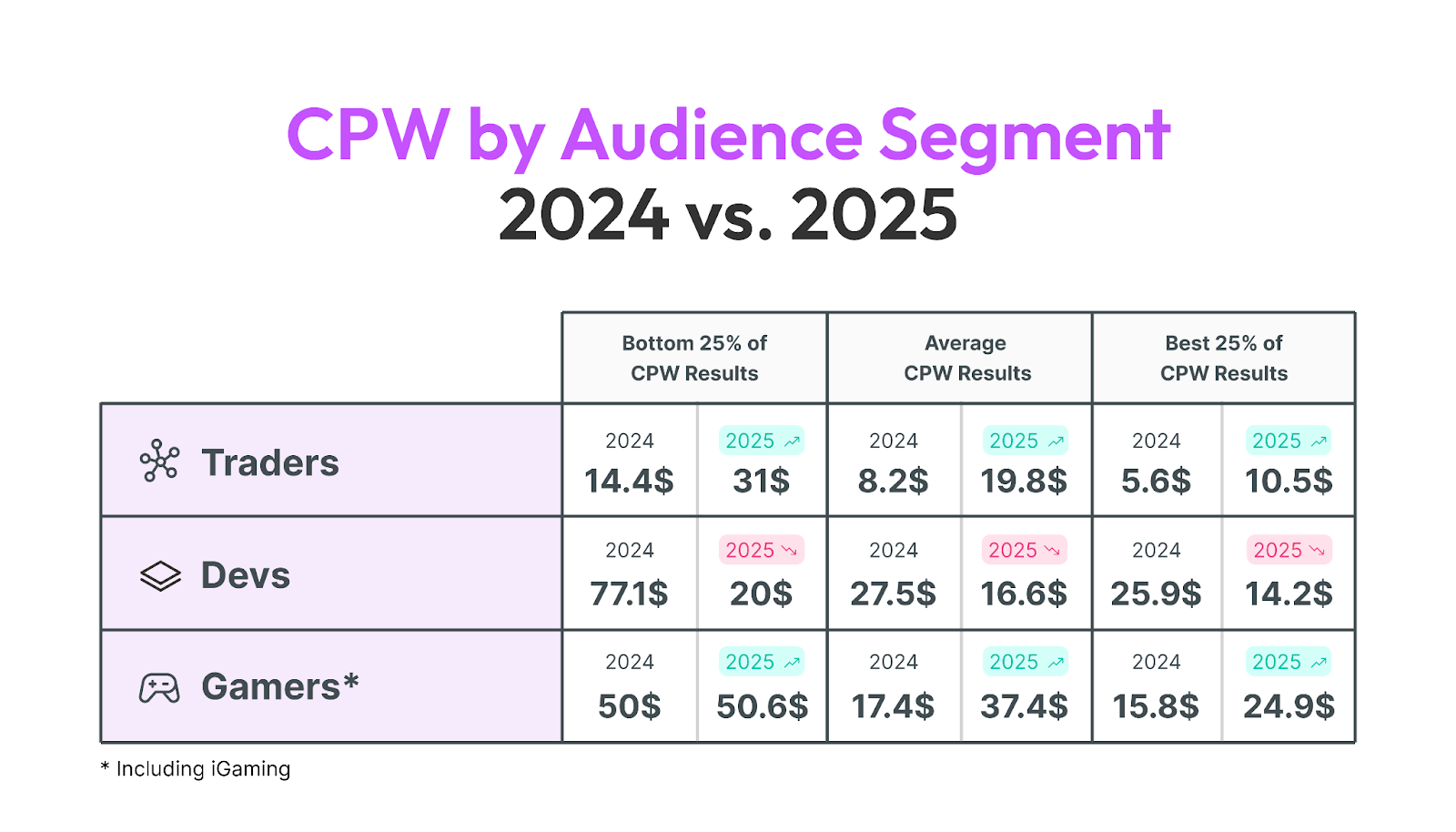

Audience Intent: Not All Crypto Users Are Equal in CPW

Looking at 2025 vs. 2024 by audience makes one thing clear: CPW isn’t just about cost. It’s about intent. Different audiences don’t just price differently. They behave differently.

Traders are the clearest signal of monetization.

They remain the most expensive audience across the board. For the top 25% of campaigns, CPW more than doubled YoY, from $14.4 to $31. Even the average trader CPW rose from $8.2 to $19.8, while the bottom 25% nearly doubled from $5.6 to $10.5. This isn’t inefficient. It's a competition. Traders convert, retain, and monetize, so demand concentrates there and prices follow. High CPW here isn’t failure. It’s priced demand.

Developers tell the opposite story: normalization.

Across all cohorts, CPW for dev audiences fell materially. Top campaigns dropped from $77.1 to $20, average from $27.5 to $16.6, and even the bottom 25% declined from $25.9 to $14.2. That’s not demand disappearing. That’s hype leaving. Fewer tourist advertisers, more rational spend, lower volatility. Developer acquisition in 2025 became quieter, cheaper, and more predictable.

Gamers and gamblers remained the most execution-sensitive audience.

Top campaigns stayed flat YoY at around $50, but the average CPW more than doubled from $17.4 to $37.4, and the bottom 25% jumped from $15.8 to $24.9. This widening spread tells the story. Gaming doesn’t forgive weak execution. In 2025, mistakes here became expensive fast.

The takeaway is simple but important: choosing an audience in 2025 meant choosing a unit-economics profile. Traders cost more because they monetize. Developers got cheaper because speculation exited. Gaming amplified every execution decision, good or bad. CPW didn’t just measure performance. It revealed where real economic value actually sits.

Figure 3: CPW in 2025 for the top 25%, average, and bottom 25% of audiences targeted: traders, developers and gamers.

Summary: What CPW Signals Going Into 2026

Across $490k in spend, 45 advertisers, and more than 22k acquired wallet-bearing users, CPW in 2025 delivered a simple message: crypto acquisition has matured, and the margin for illusion is gone.

The market moved into a revenue-first phase. Growth is no longer judged by attention or narrative, but by whether users can be acquired on terms that make economic sense. At the same time, crypto users decoupled from the crypto industry itself. While new projects and funding slowed, the on-chain user base reached new highs and became increasingly valuable to companies well beyond crypto-native ones. That imbalance, demand scaling faster than supply, pushed CPW up and made it more revealing.

What emerged from the data wasn’t just higher costs, but clearer structure. Premium regions became expensive yet predictable, signaling durable demand rather than speculation. Emerging regions reset as short-term budgets exited, making them viable again for early traction and PMF validation. Strong brands consistently paid less, often less than they did a year earlier, while unknown startups absorbed 2–3× higher CPW by trying to skip trust-building and go straight to conversions. Audience intent became impossible to ignore: traders priced up because they monetized, developers normalized as hype faded, and gaming amplified every execution decision.

Taken together, CPW in 2025 stopped rewarding shortcuts and started rewarding fundamentals. It exposed where value actually sits, what kind of users justify higher costs, and when spending is a signal of strength versus a symptom of friction.

The question going into 2026 isn’t whether CPW matters.

It’s whether teams are ready to operate in a market where CPW reflects reality, not narrative.